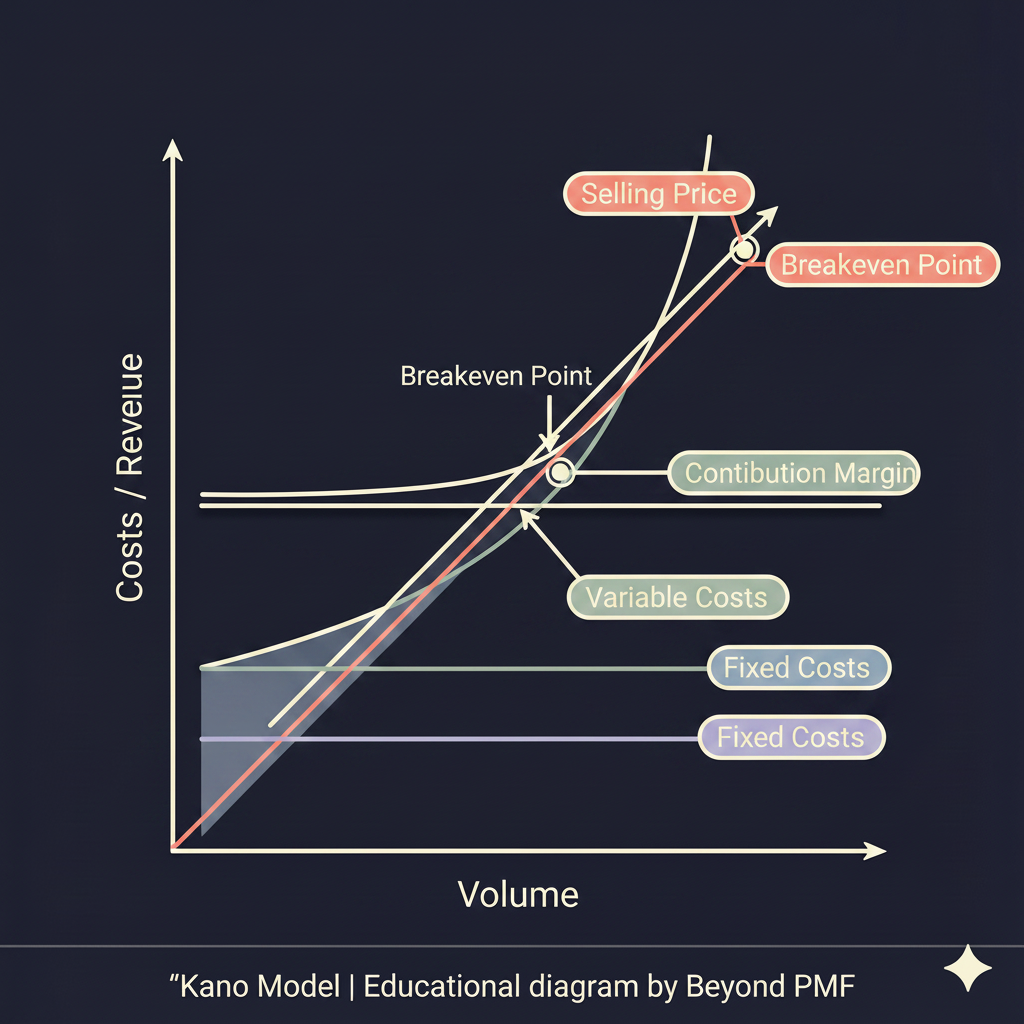

Breakeven Analysis is a critical financial calculation used to identify the point at which revenue equals the costs associated with making and selling a product, or providing a service. This analysis helps businesses understand the minimum sales volume needed to cover their fixed and variable costs, thereby aiding in decision-making and financial planning. It is particularly beneficial for assessing the viability of new products, setting appropriate price levels, and managing cost controls.