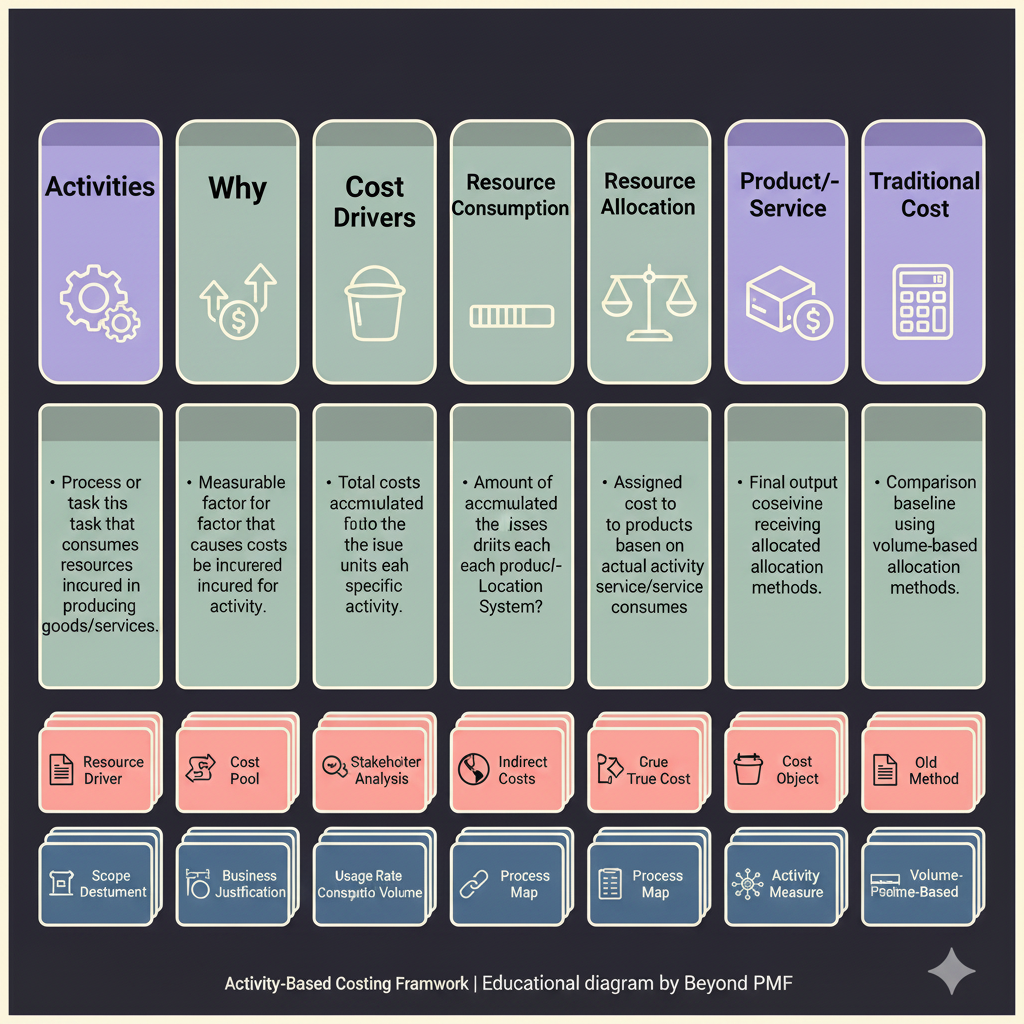

Activity-Based Costing (ABC) is a detailed accounting framework that assigns manufacturing and non-manufacturing costs to products in a more logical manner than traditional costing methods. By focusing on activities as the fundamental cost drivers, it helps organizations identify inefficient products, departments, and activities. This framework aids in understanding the true cost of producing a product, enabling more informed pricing, budgeting, and strategic decisions. The main benefit of ABC is that it provides a more accurate picture of cost behavior and product profitability.