Budgeting frameworks support planning, allocation, and governance of financial resources across products, portfolios, and initiatives. They make trade‑offs explicit and connect spending to expected outcomes and strategic priorities. These frameworks are useful in annual planning, rolling forecasts, and transformation programs where funding must follow value. Use them to improve transparency, reduce waste, and ensure investment decisions stay aligned with customer and business impact.

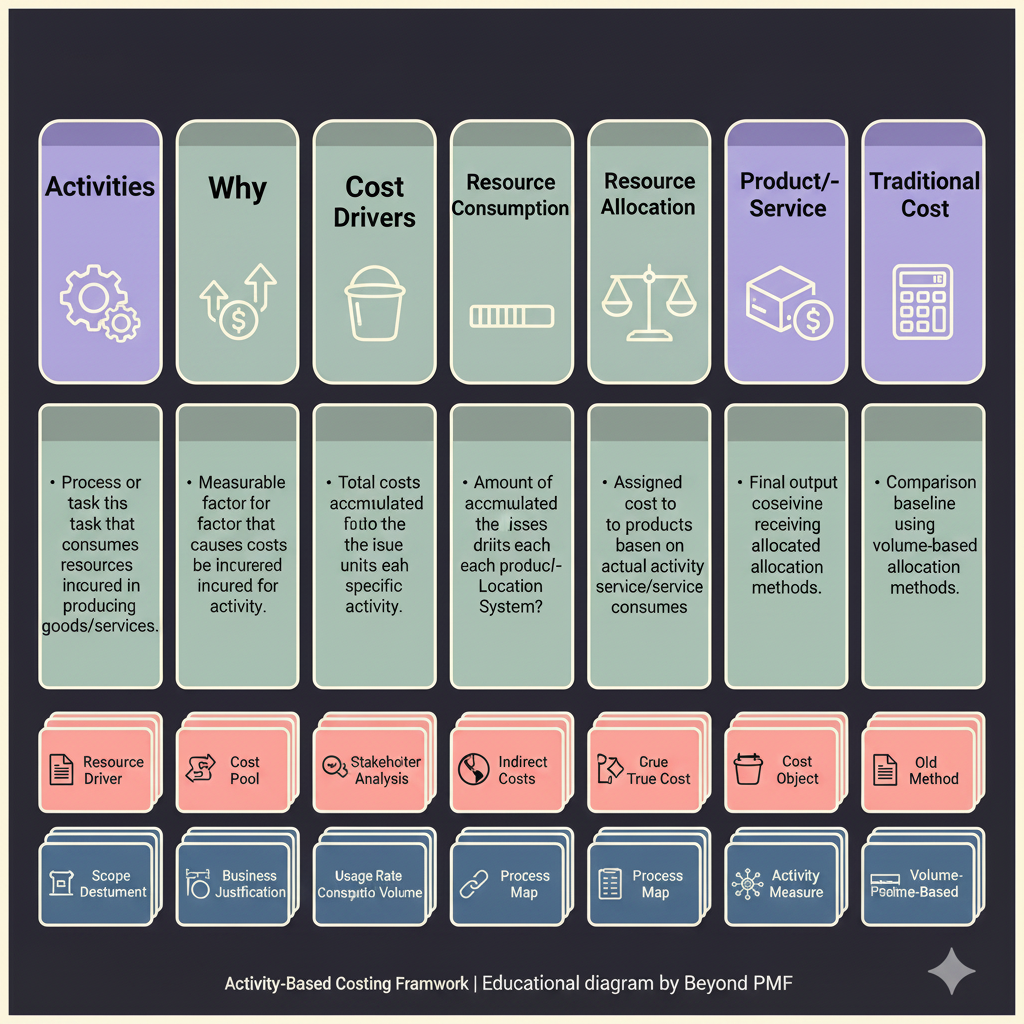

Activity-Based Costing (ABC) is a detailed accounting framework that assigns manufacturing and non-manufacturing costs to products in a more logical manner than traditional costing methods. By focusing on activities as the fundamental cost drivers, it helps organizations identify inefficient products, departments, and activities. This framework aids in understanding the true cost of producing a product, enabling more informed pricing, budgeting, and strategic decisions. The main benefit of ABC is that it provides a more accurate picture of cost behavior and product profitability.

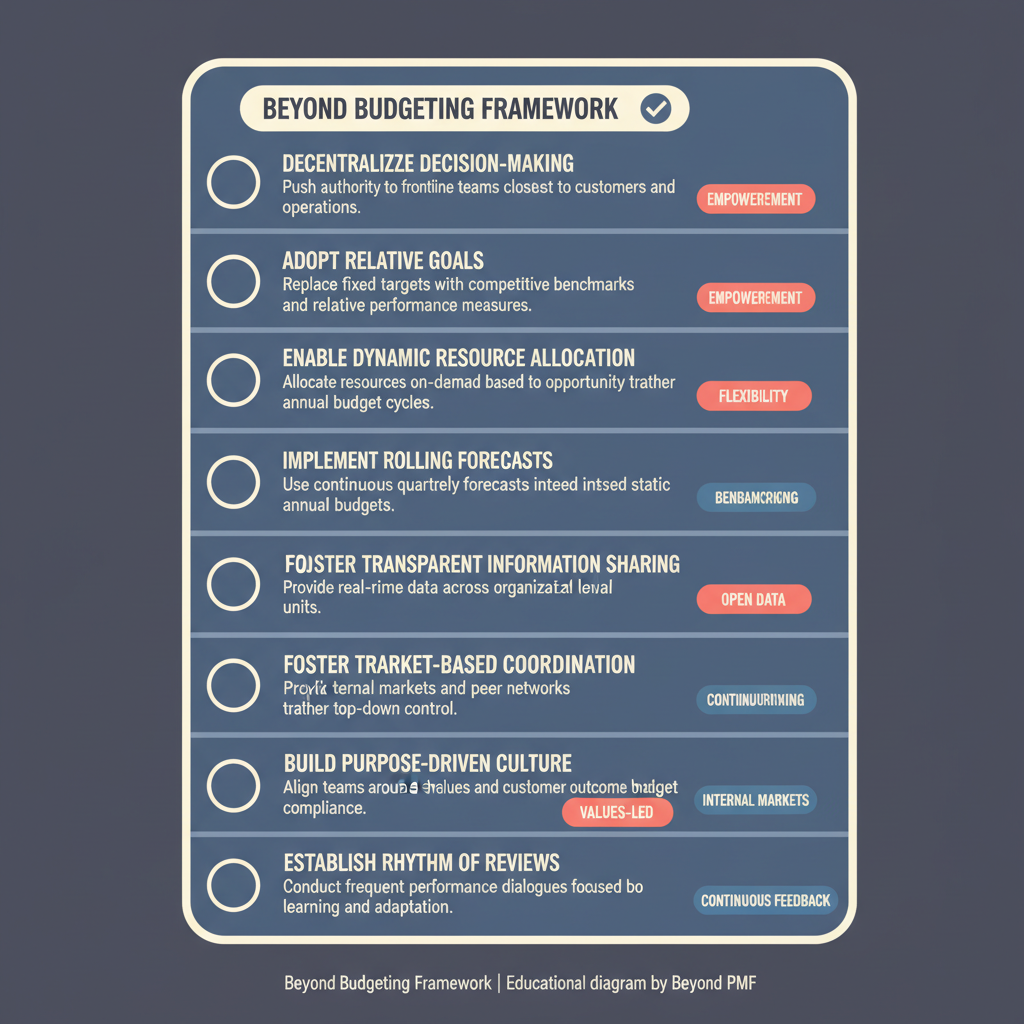

The Beyond Budgeting Framework is designed to help organizations overcome the limitations of traditional budgeting. It emphasizes a more adaptive and decentralized approach to management, focusing on fluid resource allocation and relative performance evaluation. This framework is used to increase responsiveness to market changes, foster innovation, and enhance organizational agility. Its benefits include improved speed of decision-making, increased employee empowerment, and stronger alignment with strategic goals.

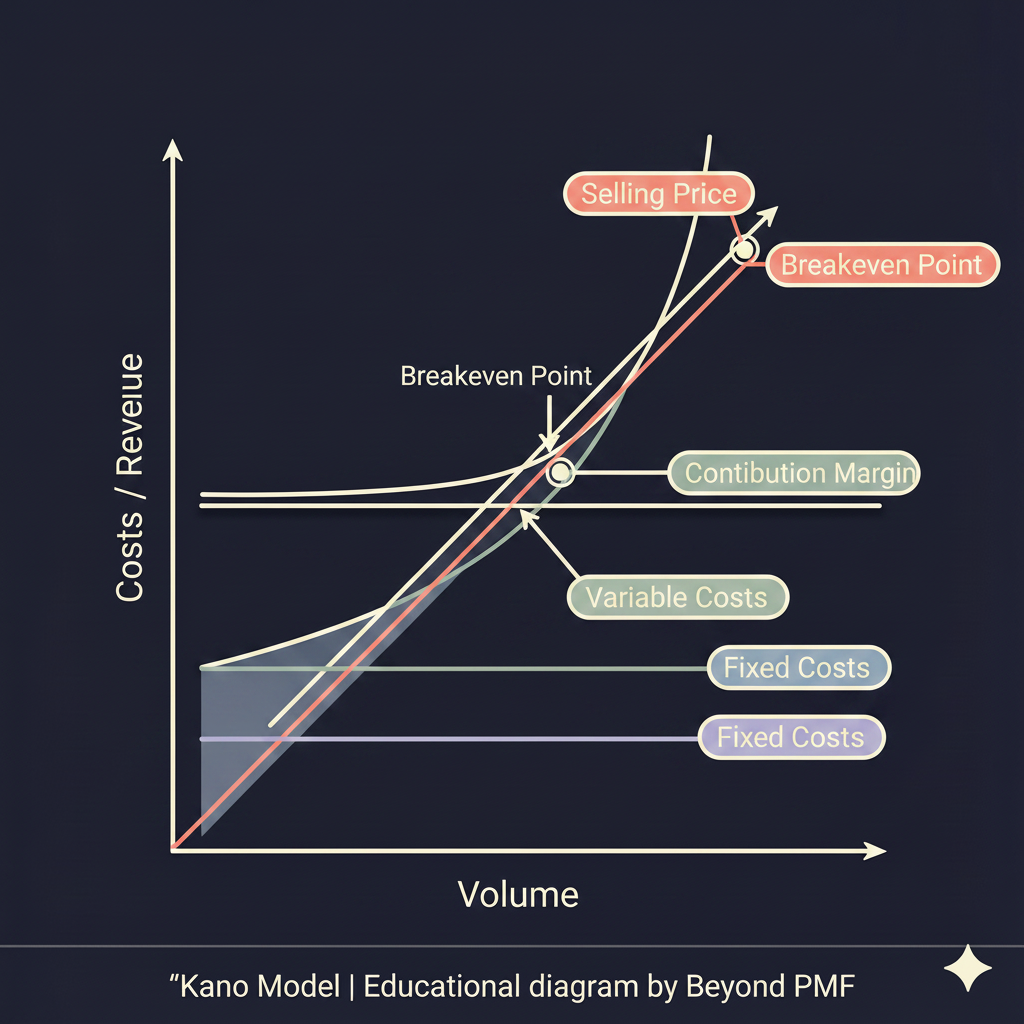

Breakeven Analysis is a critical financial calculation used to identify the point at which revenue equals the costs associated with making and selling a product, or providing a service. This analysis helps businesses understand the minimum sales volume needed to cover their fixed and variable costs, thereby aiding in decision-making and financial planning. It is particularly beneficial for assessing the viability of new products, setting appropriate price levels, and managing cost controls.

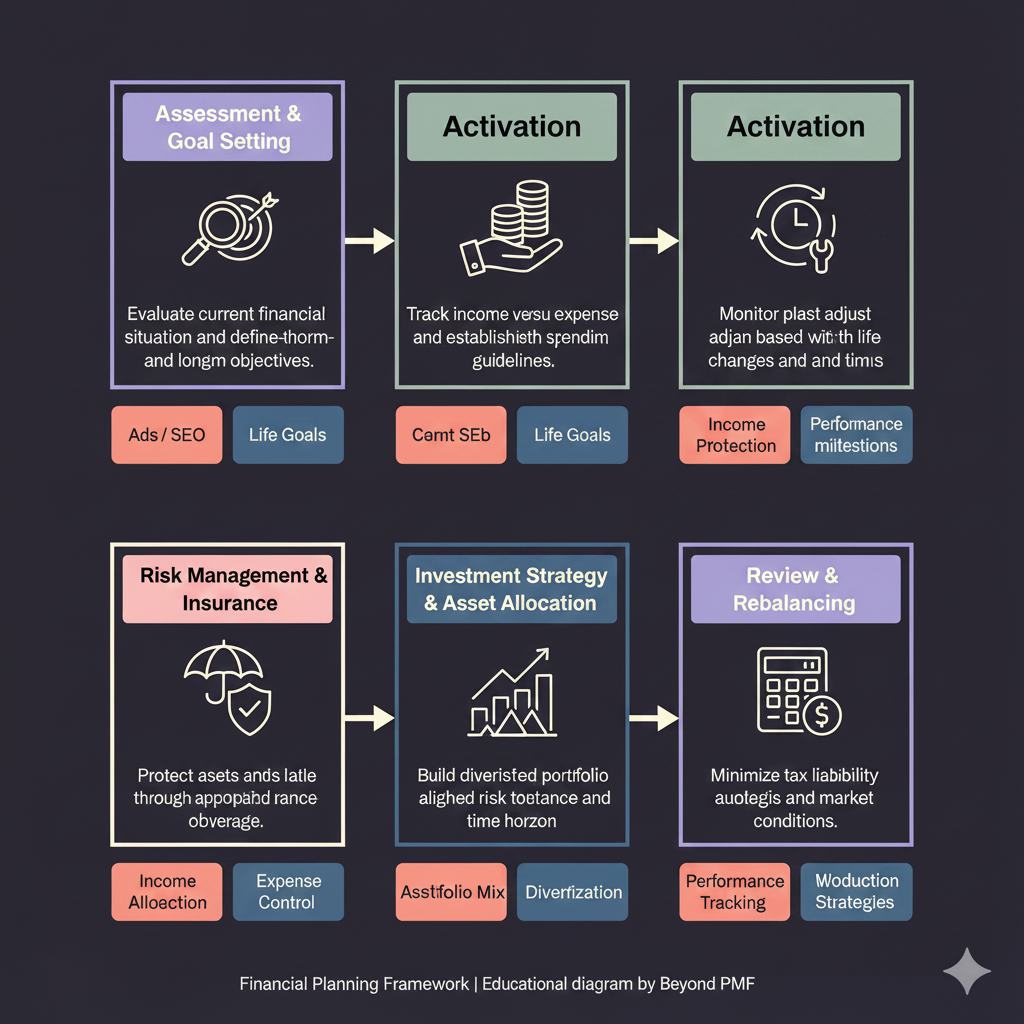

The Financial Planning Framework is a comprehensive tool used by individuals and organizations to align financial resources with their long-term goals. It involves assessing current financial status, forecasting future needs, and creating strategies to achieve financial objectives. This framework helps in optimizing budget allocation, minimizing financial risks, and ensuring sustainable growth.

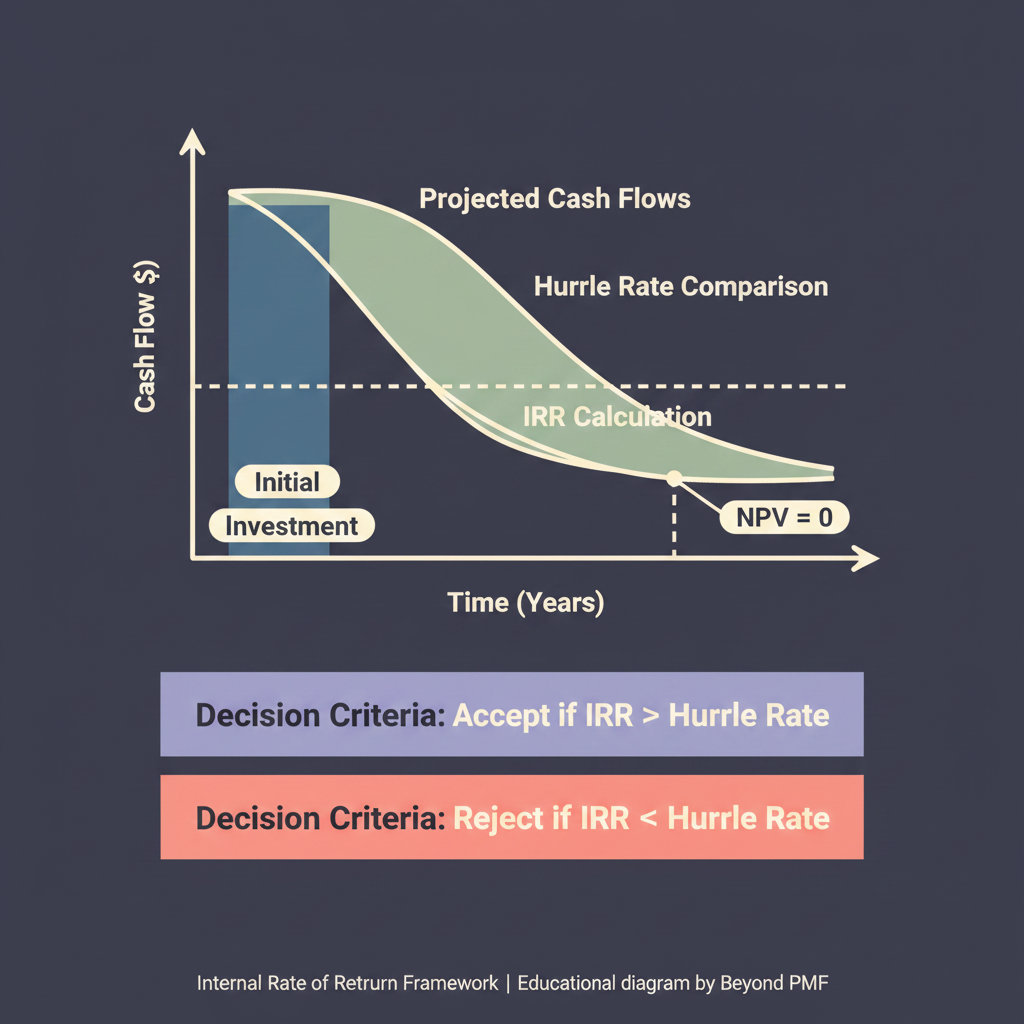

The Internal Rate of Return (IRR) framework is a critical financial metric used by businesses and investors to evaluate the profitability of investments or projects. It calculates the rate of return at which the net present value of costs (cash outflows) equals the net present value of the benefits (cash inflows). IRR is widely used because it provides a simple metric that can help compare the desirability of various investments.

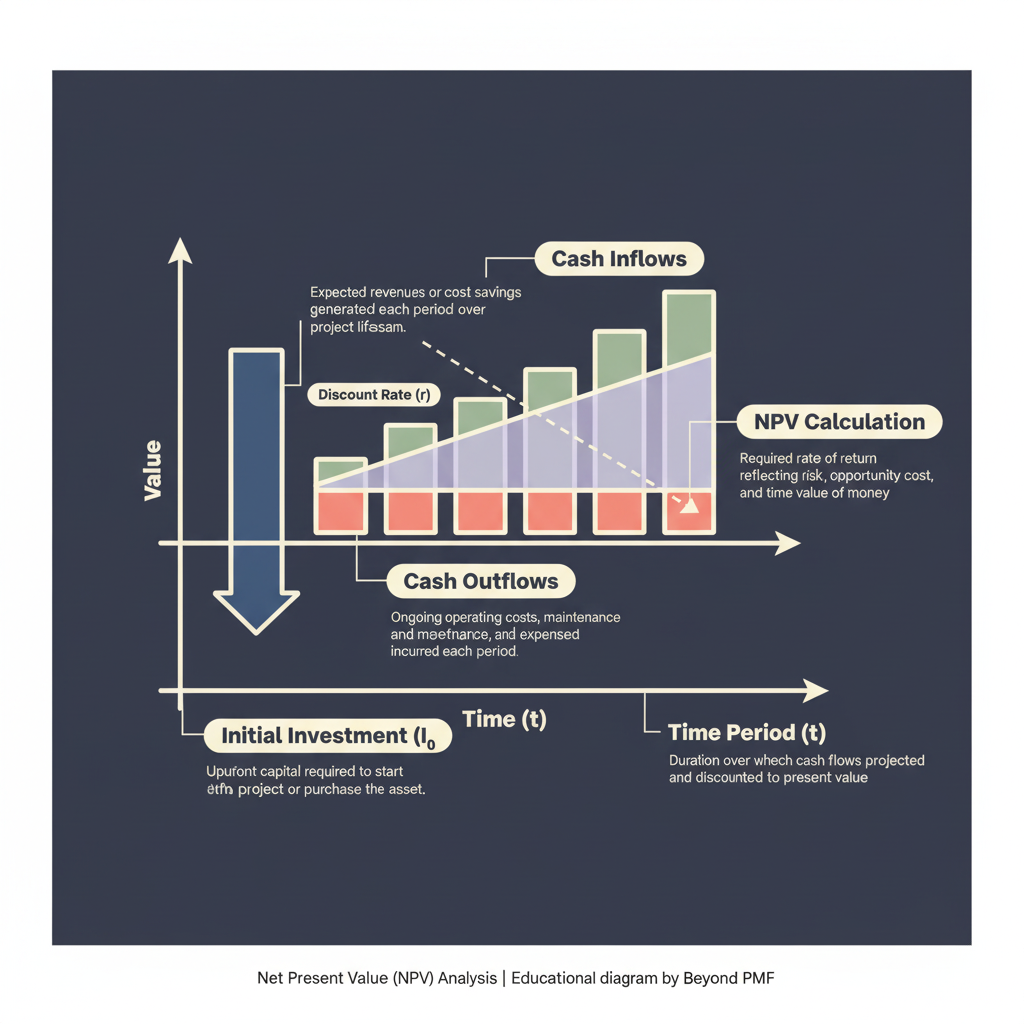

Net Present Value (NPV) Analysis is a fundamental tool in financial management and capital budgeting. It helps in determining the profitability of a project by discounting the expected cash flows to their present value and subtracting the initial investment. This framework is crucial for making informed investment decisions, as it considers the time value of money, providing a clear indicator of the financial benefit or loss from a project.

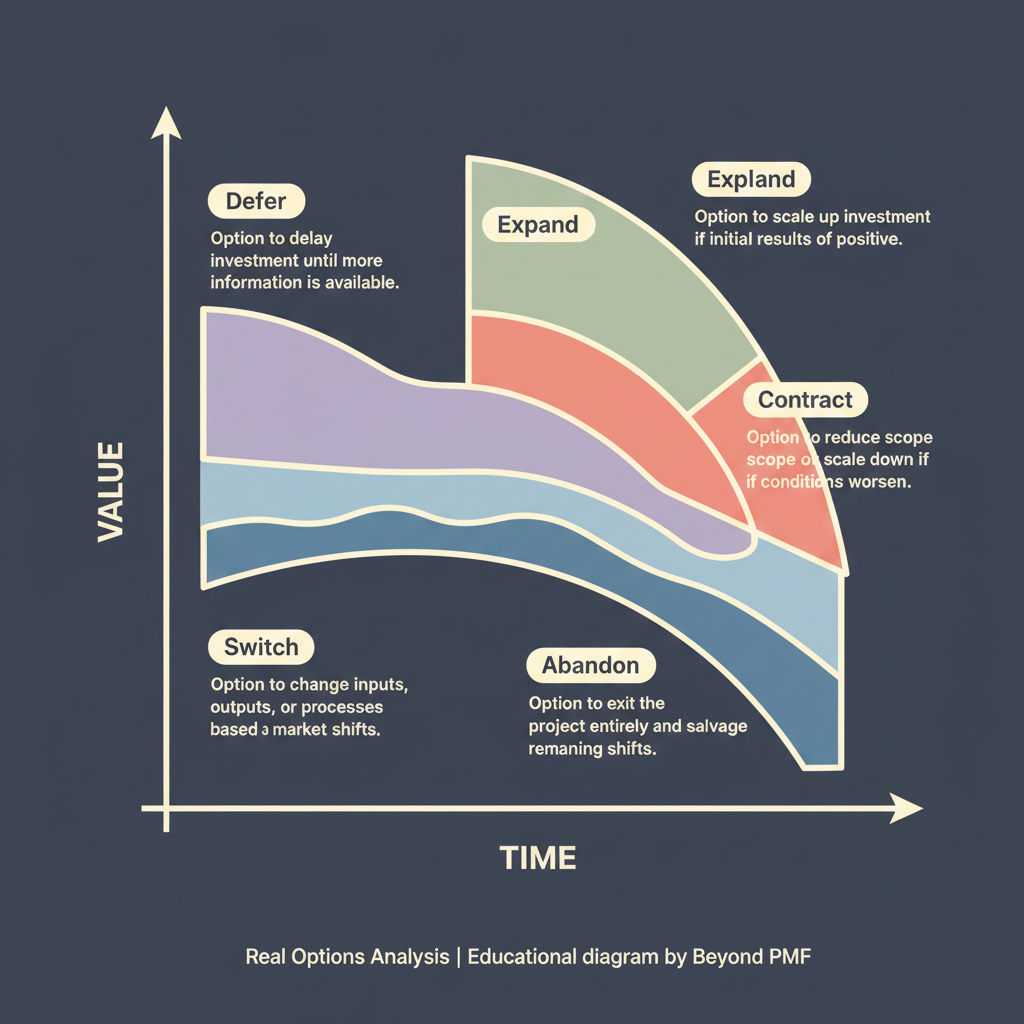

Real Options Analysis (ROA) is a framework that applies financial options theory to the valuation of options in real investments, rather than financial instruments. It is used to evaluate investment opportunities where the future is uncertain, allowing businesses to make decisions that adapt to changes in the economic environment. The approach provides a way to quantify the value of managerial flexibility to alter decisions in response to unexpected market conditions, technological changes, or competitive actions.

The Total Cost of Ownership (TCO) Model is a financial estimate framework used to help consumers and enterprise managers determine the direct and indirect costs of a product or system. It encompasses all costs, from acquisition through disposal, including procurement, maintenance, operation, and decommissioning. The TCO model is crucial for making informed purchasing decisions, optimizing spending, and minimizing unexpected expenditures over time.

Zero-Based Budgeting (ZBB) is a method of budgeting in which all expenses must be justified for each new period, as opposed to basing budgets on the previous period's budget. This approach requires managers to justify every expense and aims to allocate funds more efficiently by focusing on essential expenditures. The main benefits of ZBB include increased cost efficiency, enhanced organizational agility, and a greater alignment between company resources and strategic goals.