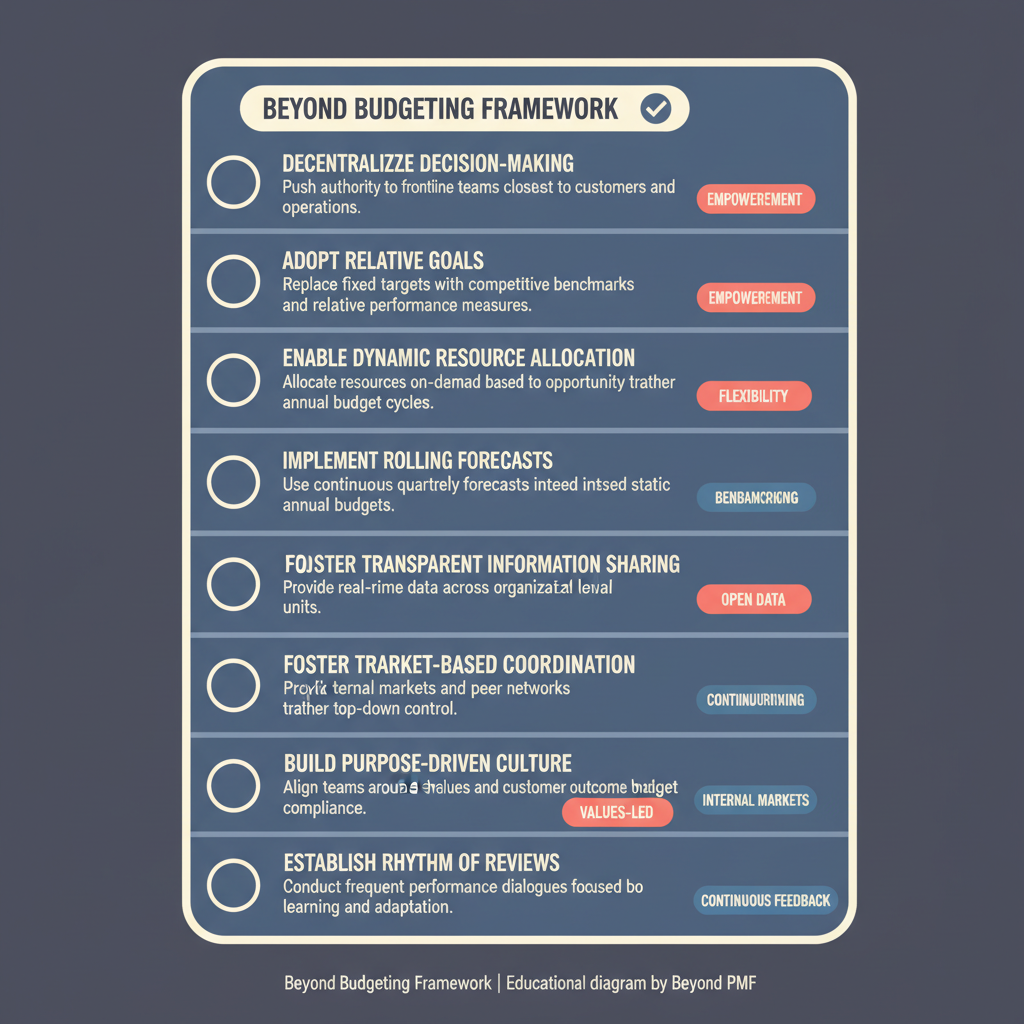

The Beyond Budgeting Framework is designed to help organizations overcome the limitations of traditional budgeting. It emphasizes a more adaptive and decentralized approach to management, focusing on fluid resource allocation and relative performance evaluation. This framework is used to increase responsiveness to market changes, foster innovation, and enhance organizational agility. Its benefits include improved speed of decision-making, increased employee empowerment, and stronger alignment with strategic goals.