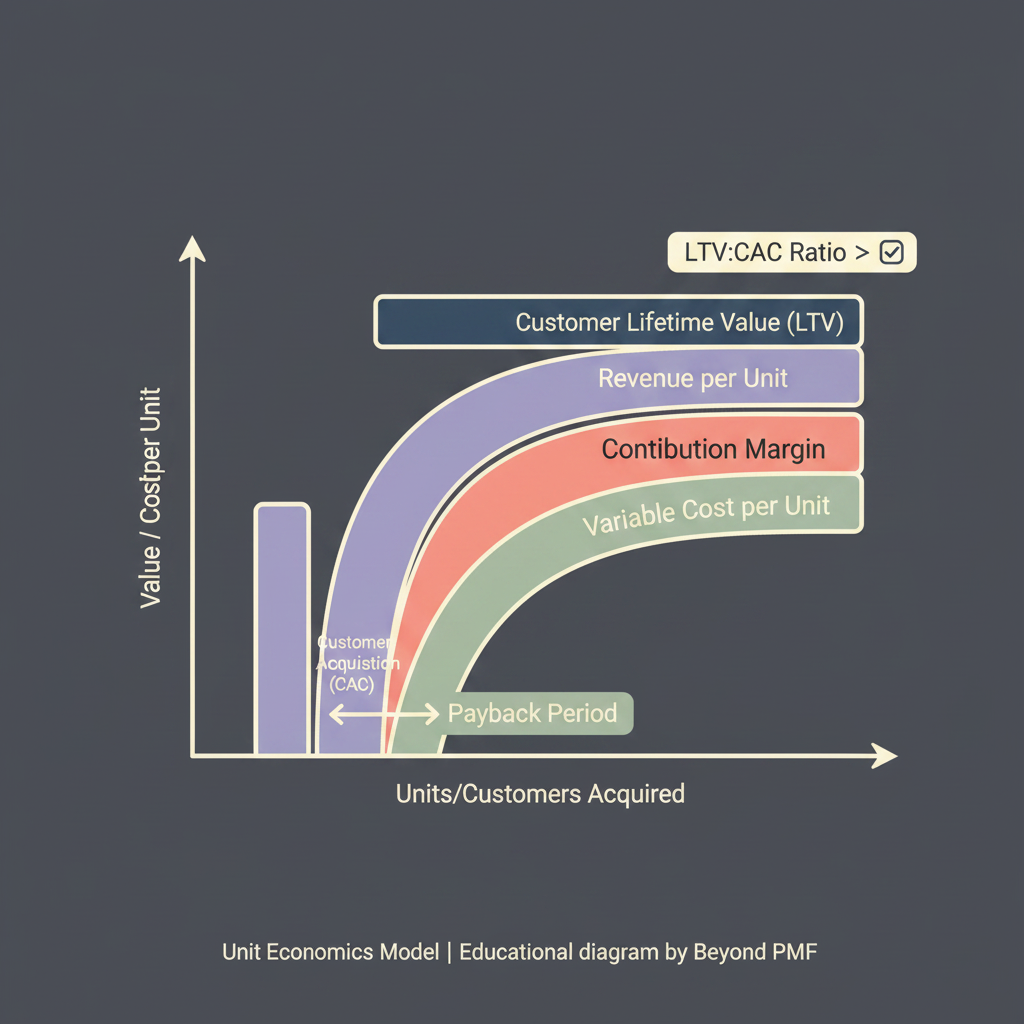

The Unit Economics Model focuses on the profitability of a single unit of product or service sold by a company. It calculates the revenue and costs associated with one unit, providing insights into the direct revenues and costs related to a product or service. This model is crucial for businesses to determine whether their products are financially viable on a per-unit basis. It helps in pricing strategies, cost management, and overall financial planning, making it a fundamental tool for startups and established businesses alike.