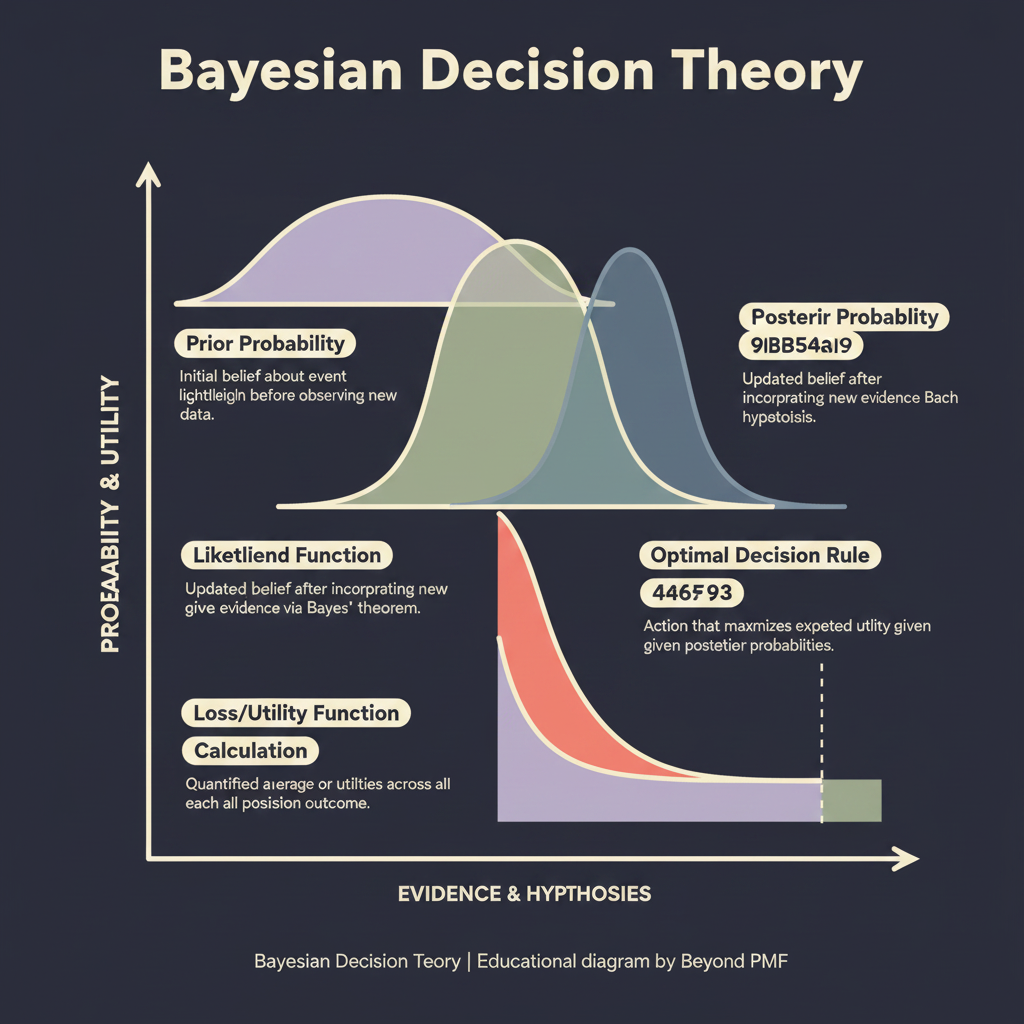

Bayesian Decision Theory is a framework that combines Bayesian inference and decision theory. It is used to make optimal decisions by updating beliefs based on new evidence and calculating the expected utility of different actions. This approach is particularly beneficial in complex decision-making environments where the probabilities of outcomes are uncertain and continuously updated as new data becomes available.